They say it takes 21 days to make or break a habit.

They also say that by mid-January, most New Year’s resolutions have already been abandoned. Gym attendance drops. Diets loosen. Optimism fades just a bit.

Markets, of course, are indifferent to all of this.

But the timing is still useful. Three weeks into the year is often when clarity replaces motivation. And in wealth management, clarity tends to matter far more.

Rather than broad resolutions or generic financial advice, this is a short list of specific things worth revisiting this year, depending on where you are financially. Not because January demands it, but because these are the kinds of decisions that quietly compound over time.

This morning I had the pleasure of speaking at the Seal Beach Chamber of Commerce breakfast at the Beach House … a room full of business owners, community leaders, and friends. For those who don’t know me, I’m Matt Pixa, founder of My Portfolio Guide, LLC, an independent fee-only wealth management firm. I’ve been honored to serve on the Chamber’s Board of Directors in the past, and was named 2021 Businessperson of the Year. While my schedule doesn’t allow me to attend as often as I’d like, it’s always a privilege to come back, reconnect, and hopefully provide a few takeaways that help people make smarter financial decisions.

Instead of giving a 15-minute “commercial” about my firm, I wanted to do something more interactive. So I asked everyone to take one of my business cards, flip it over, and write down the word RETIRE. Each letter became a conversation point for one of the six key areas of financial planning every person should be thinking about — no matter their age or stage of life.

These are the pillars that determine whether your financial plan can withstand market volatility, economic uncertainty, and life’s inevitable curveballs. If you missed the breakfast, here’s a recap of the discussion (and yes, you can watch the full 18-minute video below).

And so are we… The world stopped pretty much everything at one point during the pandemic and sports were of course no exception. For true sports fans there was nothing more depressing than watching cornhole tournaments or empty arenas void of fans, sounds, and energy. Even if you don’t like or follow college basketball, we think you’ll enjoy what we pioneered and have put together.

We’re proud to say that My Portfolio Guide, LLC was the first investment firm to publish a March Madness investing bracket where we share our picks and match them up against each other. We break down and assign each of the four “regions” with an asset class and then pick teams (stocks) that we think have the best chance at doing well relative to others.

Not only is this “exercise” a way for us to share our ideas from a macro perspective, but it offers a fun platform to dig into a couple specific investments and themes we are following or excited about in the year ahead.

Click here or below to enlarge and see the entire bracket for 2023.

You’ve behaved fairly well after some insanely raucous behavior last year. You (the market) has actually surprised a lot of folks just barely six weeks into the year. While there is plenty of calendar left in 2023, we’re watching you and it’s simply interesting to see that half the room doesn’t trust your next move while the other half wants to… but still can’t!

The books are closed on 2022, and what a year it was! The past few years have brought the word “unprecedented” to a whole new level. Both stocks and bonds were down in 2022, which is extremely rare and actually only happened twice in the past 100 years! (1931 and 1969). We won’t rehash it all but it’s not just that stocks were down almost -20%, but rather that what was supposed to offset some of that drawdown, never did. Historically bonds have basically always mitigated some of the pain of stocks getting tattered but not last year. 10-year treasury bonds were also down -15% and if you want real pain, 30 year bonds got torched by almost -30%. Name a stretch in your lifetime that was worse? Even if you’re 90 years old…you can’t.

So, enough about what has happened but our focus today is on how this plays with your mind. Below we’ve written a list of all the financial media talking heads as well as economic experts who are notpredicting a major recession. Look through our extensive list of names and what do you see?

Oh wait…there are no names listed. Feel free to comment below or let us know if we missed anyone but rarely have we ever seen such an environment of groupthink that it begs the question…what if they’re all wrong? There have been some major economists who in times past have really missed the mark but for some reason they still have a platform and the ability to get your attention. In a future article (or letter to you, Mr. Market) we’ll do a little report card on all the “gurus” who somehow still command everyone’s eyeballs but often can’t correctly guess how many fingers they have. OK…perhaps we’re laying it on a little thick here but hopefully you get the point. There is too much groupthink going on right now and it’s times like these when it pays to take a little bit of a contrarian view.

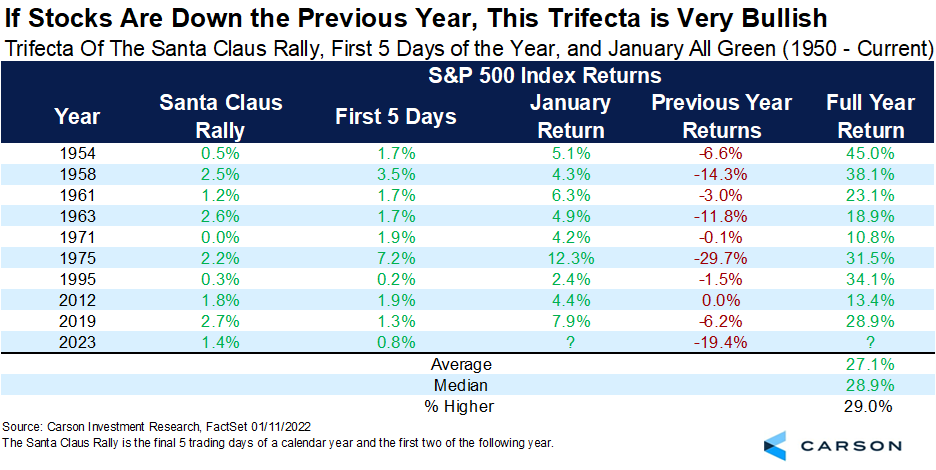

We wrapped up January in surprisingly good fashion (again…almost everyone got it wrong but we’ll modestly remind clients we did not). Couple that with what is the proverbial “Santa Claus” rally period and you have some interesting history to look at. When stocks are lower the year prior, but gained during the Santa Claus period and first five days of January…we’ve seen a market average +27% the next year. Could it happen this time? Maybe not to that extent but if it doesn’t it will be the first time ever it didn’t at least go higher (nine for nine prior).

Now nobody said it would be smooth sailing (it rarely is). Expect a bit of a cooling down period as we now digest Q4 earnings season until month end. It also happens to be seasonally be a time for a natural pause or break with the back half of February being historically weak.

Regardless, barring some major unexpected calamity, this likely pause in the markets is a perfect opportunity to not only catch your breath (with Mr. Market) but also take a few chips off the table in areas you’ve been wishing you had earlier. For example, most people who had way too much tech on the way up got slaughtered in 2022 with the Nasdaq peeling off -33%. Now that we’ve seen a nice bump in tech stocks to start the year, why not sell some and reallocate to another area?

If you read the recent quarterly newsletter from My Portfolio Guide, LLC, you’ll note the areas we still like. Commodities are down to start the year…what a great place to be building a hedge if you missed their run-up prior. Along those same lines, what also helped our model portfolios last year (relative to what most people had outside of stocks and bonds) was gold. The dollar will retreat some more (unhitching the trailer) so we couldn’t be more bullish on gold being a key component in this environment. One more area that has slumped a bit to start the year are oil stocks (another rare bright spot in 2022). In typical human and emotional fashion, people somehow don’t want single digit multiple (i.e. cheap!) stocks with high yielding dividends. What’s not to like?!? Even Joe Biden told us earlier this week during the State of the Union that we’ll need oil for at least another 10 years…

Lastly, if you’re in the mood on making bets….Here’s a tip for all those watching the Super Bowl this Sunday. If you don’t have a dog in the hunt and are simply “hoping for a good game”…change your tune right now; you should want a blowout (perhaps not for entertainment value but for the market). In years when there is a single digit win during the Super Bowl the market only averages +5% and higher less than 60% of the time. However, on years with double digit margins of victory the market averages +11% and a 79% chance of going higher.

As silly as the “Super Bowl Indicator” is by the way, we did write about it last year (click here) and true to form…perhaps that’s why the market got drilled (kidding!). The Eagles are slight favorites but if you’re just an investment geek and want to root for a team…the football Gods all say the Chiefs need to win and ideally by 10 points or more. It likely won’t happen so enjoy the game and those expensive commercials. By the way, they used to cost advertisers a cool $1 million a few years ago for a primetime spot but are now upwards of $7 million! (and we have the gall to complain about $7 eggs?!?)

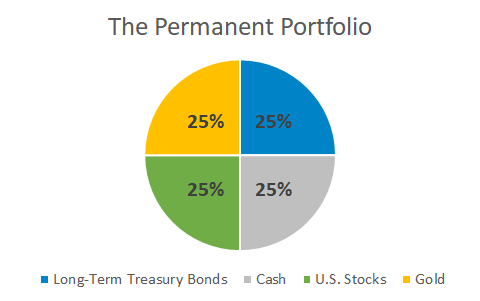

In a year where the stock market has provided zero safe places to hide…you may have changed, the markets certainly have, but one thing has not; the Permanent Portfolio.

We’ve reviewed the Permanent Portfolio before but believe it’s time to check in and provide an update on how it’s doing relative to the broad markets now as well as chime in on whether the strategy still has merit going forward. For some quick background, our first original review was written in June of 2013 (click here to see that). Most recently we revisited the topic with an update in November of 2020 (click here) as we climbed out of one of the wildest years in world history amidst a global pandemic.

If you didn’t hit the embedded article links above, the Permanent Portfolio is pretty simple at face value. The Permanent Portfolio is a seemingly basic portfolio allocation strategy created by investment advisor Harry Browne in the 1980’s and outlined in his book Fail-Safe Investing back in 2001. Here’s the secret (simple) sauce and how each asset class should do during repeatable economic cycles:

Journalists write about you daily. Investors constantly think and talk about you. Analysts and economists spend their entire careers trying to figure you out. You’re a complex yet simple character, Mr. Market! All that said, today we want to share with our readers a substantial part of you that doesn’t get enough appreciation (pun intended). Let’s talk dividends!

That’s exactly where we’re at right now. We’re not going to wait for the financial media to announce it or tell us that it’s only a bear market if we officially drop -20% or more. The intent of this article is to explain not only what a real bear market is, and how this one has behaved differently, but also what to do next.

We’ll open this letter to our friend “Mr. Market” by stating one thing that will be very obvious in six to 12 months. 90% of people reading this article will have gotten it wrong. It’s not your fault though…it’s the way our minds are wired and the content we’re constantly being fed.

Regardless of your current market strategy it’s times like this that will test the most patient of long-term investors. We’ve written about this countless times but no matter what the sage counsel or stock market adage is, you should be rattled right now. We could be like most “perma-bull” financial advisors and try to data mine for all the reasons to stay calm or share positive anecdotes to convince you that now is the time to invest; it won’t matter though. Putting “lipstick on a pig” won’t help you nor the current market environment. Bad news and reasons to panic will be the headline for the weeks to come and there will seemingly be no safe place to hide.

Does the old stock market adage of “sell in May and go away” make sense? We’ve actually written about this one spring about nine years ago where we actually advocated taking some chips off the table, however it had less to do with a cute stock market rhyme and more due to profit taking. Where are we at now going into May and is this allegedly poor seasonal time of year appropriate to sell or perhaps not?