Dear Mr. Market:

Chalk it up to the “dog days of summer” but we haven’t written a letter to you in a while. Perhaps this is in part to the wild ride you’ve sent investors on since the whipsaw action and insane volatility we saw this past December. For those of us with short-term memory issues, the year ended in brutal fashion with the worst December in 80 years. If you sold out of your investments, threw in the towel and fell prey to your emotions, you then missed the best January the stock market has seen in 80 years.

If you still haven’t paid much attention then perhaps the opening of this past week also hasn’t phased you…or should it?!

We’re often reminded of a famous quote when thinking about stock market corrections:

“More money has been lost in trying to time a correction than has ever been lost in the correction itself” -Peter Lynch

The larger question for most should be not one of stock market corrections and how to navigate them but rather are we truly headed for a recession?

This past Wednesday the Federal Reserve cut interest rates by 0.25% with a statement of “global developments” and “muted inflation” being the major influencing decisions. Where most people are left to continue guessing is whether this was a ‘one and done’ type move by the Fed or the first in a series? While many economists and “experts” are predicting three cuts this year we personally are in the camp that only one more cut is likely and furthermore the European Central Bank along with the Bank of Japan will also follow suit in this easing trend.

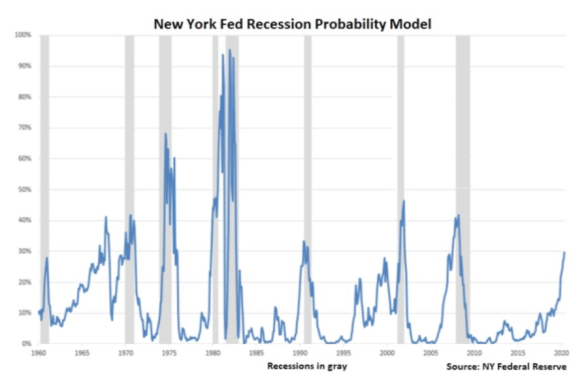

There are indeed signs of an economic slowdown, specifically in manufacturing data, but we still see our domestic economy in a modest expansion mode. People that are pounding the table of an already existing recession need to revisit the actual definition of one. While a general slowdown can often take place long before a recession officially starts but there still needs to be two consecutive quarters (six months) of GDP contraction and negative growth to warrant such a call.

Below we share the “New York Fed Recession Probability Model” going back with 60 years of data.

The other huge headwind or “elephant in the room” is of course the US-China trade tensions. While this headline is nothing new to the markets we saw more volatility and worrisome action after the White House announced an additional 10% tariff on another $300 billion of goods coming from China beginning September 1st.

Lastly, added to these well telegraphed headlines are the ongoing geopolitical conflicts with Iran. All of these issues coupled together certainly present concern and increased stress on the markets but the general probability of a US recession in the near-term remains reasonably low over the remainder of the year. We are indeed in a late cycle of economic expansion but believe these fears tend to get overstated and we still have a bit more room to run.

In the meantime, let this letter to “Dear Mr. Market” serve as a reminder that just because someone tells you we are in a recession does not mean we are anywhere close to one. Very few recessions happen during the time the general consensus predicts them. Nobody has correctly predicted recessions with any level of consistency so no matter how convincing their story is now, it’s still unproven to be statistically reliable.