Dear Mr. Market:

Dear Mr. Market:

The equity markets typically dominate the headlines but recently there has been more and more talk about the Fed and where interest rates are going. Stocks are definitely a more intriguing topic as they can move very quickly in either direction and make a dramatic impact on investor’s portfolios. Future Fed activity will have an impact on what is often the most neglected portion of a portfolio – Fixed Income or Bonds.

Most investors spend a minimal amount of time with this portion of their asset allocation. It is often the textbook definition of a ‘buy and hold’ approach and why shouldn’t it be? For the last several years investors have accepted the fact that interest rates are essentially zero and this portion of their portfolio warrants little to no attention. While this approach has been adequate investors that subscribe to this approach could find themselves with losses in what they consider their ‘sleep at night’ portion of the portfolio. When and if the Fed makes any changes to their policy investors need to be prepared to make changes to this portion of their investment portfolio.

When rates do change the behavior of bonds can be explained using something that everyone has seen on a children’s playground…a seesaw or teeter-totter. It is based on a very basic concept – when one side goes up the other will go down. When using this analogy with Fixed Income, one side would have interest rates and the other would have the principal value of the bond or fund. As rates go down the principal would go up and if rates go up the principal would decline. Fairly straightforward…isn’t it? Additionally, the further away you are from the middle of the seesaw (fulcrum point) the harder your landing will be. This playground explanation paints a simplistic explanation of how the price of bonds is affected by interest rate changes but what should you focus on when it comes to your fixed income positions?

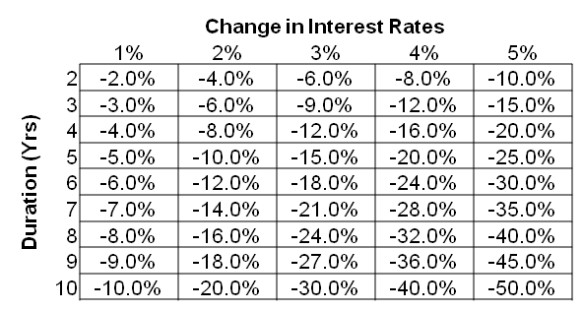

Duration – An indicator that illustrates how the price of a bond will be impacted with a change in interest rates. The calculation itself is semi-complicated but this indicator is considered standard data when looking at bond bond funds and ETFs. It is expressed in years; the higher the number, the greater the interest-rate risk or reward associated with bond prices.

How much might you lose when interest rates increase? It’s not hard to see once you lay out the rate increase compared to the duration of your bond investment. For example: If rates increase 2% and the duration of your bond investment is 3% you will see -6% in value. If the same rate increase of 2% occurs but you have a duration of 9% you could see a decline in value of -18%.

Expenses – Any additional charges/fees make an impact on a portfolio but they are particularly important when looking at fixed income, especially in this low interest rate environment. Remember that higher expenses do not correlate to higher returns. Investing is the one area where the old adage of “you get what you pay for” is sometimes the absolute opposite.

Don’t chase yields – Generally a higher yield indicates a higher risk. Look at the credit quality to fully understand the risk associated with an investment.

Don’t duplicate funds – Two funds might have different names or parent companies associated with them but when you look at the holdings they basically duplicate each other. A diversified fund can offer exposure to numerous sectors within the fixed income universe.

Credit Risk – Remember a bond is a loan. Credit risk is the chance that you will not be paid back as the lender. Anything below a BBB rating is considered below “investment grade”.

If you haven’t reviewed your bond positions now could be the ideal time. There are a multitude of options to consider and you now have more cost effective options than there were available just five years ago. There are many factors that investors need to consider on both the domestic and international stage when it comes to fixed income. The most important thing for investors to remember is why they have a portion of their portfolio allocated to fixed income – to help manage overall portfolio risk. Investors typically look at their equity positions frequently and pass over the fixed income portion of their portfolio. When was the last time you gave your fixed income an in-depth review?

Pingback: Dear Mr. Market: