We can’t tell you how many times we have heard investors say something along the lines of, “I have this annuity that I was talked into years ago, I don’t really understand it and I haven’t heard from the guy I bought it from since”.  Annuities are one of the most misunderstood and possibly abused financial products in the financial services industry today. They are layered in promises that are far too often not delivered to the individual that purchased the annuity. While they look simple in nature they are actually quite complex and it is vital that investors conduct their own due diligence and research before purchasing any annuity product.

Annuities are one of the most misunderstood and possibly abused financial products in the financial services industry today. They are layered in promises that are far too often not delivered to the individual that purchased the annuity. While they look simple in nature they are actually quite complex and it is vital that investors conduct their own due diligence and research before purchasing any annuity product.

The basic structure of an annuity is quite simple; the investor deposits money with an insurance company either in a lump sum or with scheduled periodic payments over several years. In return the investor will receive a stream of payments either immediately or in the future for a set period of time. The terms and conditions can vary from company to company and there are many different types of annuities and features that can be added to them. It is important to always remember that an annuity is a contract between an insurance company and an individual for certain guarantees and that they should never be viewed as investments! We will attempt to dig in a bit deeper and offer an overview of annuities that will empower investors to make educated and informed decisions.

Types of Annuities:

Over the years insurance companies have introduced many different types of annuities along with multiple features and benefits that can be added to the annuity contracts. Below are some of the most common types of annuities available to individuals today:

Deferred Annuity: Individuals make payments into an annuity over a period of time. Typically annuities have two different stages – accumulation and annuitization. In the accumulation stage funds are deposited into the account, at the end of that stage the investor can annuitize the account and convert the funds into scheduled payments creating a stream of income.

Immediate Annuity: These are purchased with a lump sum in exchange for scheduled payments that are to be received immediately.

Fixed Annuities: These annuities will guarantee a fixed or minimum interest rate over a set period of time. The rate associated with these annuities will reset on a pre-determined time frame based on the current interest rate environment. The terms and rates will vary from each company.

Variable Annuities: These annuities offer exposure to the stock market (equities), bonds and cash. They typically will offer a variety of mutual funds (also called sub-accounts); the investor can choose their allocation within the annuity much like a 401(k) retirement plan. Some contracts today offer a guaranteed minimum rate of return and can lock in gains at each anniversary date (these features are offered with an additional fees).

Equity Indexed Annuities: These annuities are tied to an index or benchmark such as the S&P 500.

Fees and Expenses

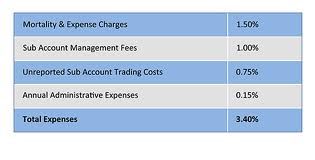

We often hear that investors are overwhelmed when they receive the prospectus or contract associated with an annuity and begin to read through the information, particularly when they begin to look at the various fees and expenses. Annuities can have layers upon layers of fees and it is often challenging to calculate what the total expenses are. Below are a few of the more common fees that investors can expect to encounter with annuities:

Operating and Administrative Fees: Essentially these are maintenance fees that cover administrative expenses, bookkeeping, reporting and other miscellaneous fees from the insurance company.

Mortality and Expense Fees: When an insurance company accepts an annuity contract they are assuming risk and they charge a fee for this.

Guaranteed Minimum Death Benefit: This is usually an optional feature or ‘rider’ that can be added to an annuity. It provides a specified amount to beneficiaries if the annuity owner dies before the contract ends.

Guaranteed Lifetime Withdrawal Benefit: This feature or ‘rider’ will deliver a guaranteed stream of income for the remainder of the owner’s life. This is typically a percentage of the principal or value of the contract when the annuity is annuitized. As with all of these features there is an additional fee charged for this.

Sub-Account Expenses: These are essentially the operating expenses associated with the investments that are available in a variable annuity. For each sub-account (mutual fund) held within an annuity there is a fee charged on an annual basis.

Surrender Fees: Deferred annuities can have additional charges including surrender fees. A surrender fee is a penalty for withdrawing money before the designated surrender period has expired. This timeframe is typically 7 years but can be longer. The fee is a percentage of the withdrawal amount and in most contracts will decline over the surrender period. The standard structure is a fee of 7% in the first year and they decline one percent each year until the surrender period is over.

There are many other miscellaneous fees associated with annuities. While they might not look like they are significant on an individual basis they can add up very quickly. It is not uncommon to see an annuity have total fees of 3.5% to 7% on an annual basis.

Items to consider:

While annuities have many bells and whistles to attract investors there are several key elements that need to be considered before purchasing one:

Taxes – ** We encourage anyone that has questions regarding the tax ramifications associated with an annuity to consult with a tax advisor. **

Many investors are attracted to the fact that annuities offer tax-deferred growth. Many investors don’t realize that if funds are withdrawn prior to age 59 ½ that the IRS may impose a penalty of 10%. All investment gains within the annuity are taxed at ordinary income tax rates. For many individuals this offers no advantage when compared to long-term capital gains rates. It is also important to note that death benefit payouts can be fully taxable and are not treated like a life insurance death benefit.

Death Benefits – Often we see that annuities have been loaded with additional features that essentially structure them to offer the same benefits as a life insurance policy. Investors pay for these features, which can reduce the account value over time. For example a ‘rider’ could be added to an annuity that would have a death benefit that would pay the beneficiary over a set period of time once the annuity owner dies. In many cases it would be smarter to simply buy an insurance policy as the fees would be much lower and in the long run it would be far more cost effective.

Liquidity – In a deferred annuity there is a period that investors agree to fund the account before they begin to withdraw funds from the account. This time frame is typically 7 years or more and referred to as the accumulation phase. Many contracts will allow for withdrawals during the accumulation years but if the amount is more than what is allowed per the contract the investor will pay significant penalties. It is best that investors don’t plan on accessing any of the money in an annuity for the first 7 years due to the prohibitive fee structure.

Returns – Many investors focus on the fact that there are ‘guaranteed’ returns associated with annuities but these can be very misleading. In many situations the guarantee is nothing more than a guarantee to underperform the market! A great example of this is an Equity Indexed Annuity where the returns are based on a stated index like the S&P 500. The various fees that are charged annually need to be taken into account when looking at returns. If the benchmark rose 9% and the total fee was 4% you would then post a return of 5% or a 4% underperformance. With Variable Annuities it is important that the management fee of each mutual fund be taken into account along with the performance of the manager. The difference of just a few percentage points can make a profound impact on a portfolios performance over time. The chart below illustrates the difference between an Indexed Annuity and the S&P 500:

|

Investment of $1 Million: S&P 500 vs. a hypothetical annuity |

||||

|

12/31/81 |

Time Horizon |

Annual Return |

Amount 12/31/2011 |

|

|

S&P 500 |

$1,000,000 |

30 years |

10.80% |

$21,644,281 |

|

Hypothetical Annuity |

$1,000,000 |

30 years |

7.40% |

$8,514,089 |

Companies Fundamentals – It is vital that investors look at the financial stability of the insurance company that is issuing the annuity. If the company were to fail then annuity owners may not receive all the benefits that they were expecting. There are several different companies that rate insurance companies and this information can be found online (A.M. Best & Moody’s).

While annuities can have a place in your portfolio they are certainly not a one-stop solution, as many annuity salespeople would have you believe. They are commonly referred to as one of the most abused financial products in today’s financial services industry. Every investor likes hearing that there is a promise or guarantee associated with any product, particularly with the volatility we’ve experienced over the last decade! Annuities will sell like hotcakes in volatile and uncertain markets where fear is running rampant. In markets like these the old adage of “annuities are sold not bought” could not be more true. Fear and emotion often sell the product, skillfully commissioned salespeople know this and capitalize on it.

We would encourage everyone to be cautious and do your own due diligence when looking at an annuity. One critical factor to keep in mind is that the typical producer will earn around 5% to 7% of the first year premium when an annuity is sold! They are one of the highest paying products available to producers in today’s market. Take the time to ask yourself if you are buying a product that fits into your overall financial plan or is it simply lining the pockets of an annuity salesperson?

Some key questions to ask before buying an annuity:

- Are you buying an annuity inside an IRA? This is essentially creating a double layer of tax-free growth that is not needed. Unless there are features that you desire with the annuity you are basically exposing your retirement account to additional fees and wasting your money.

- What type of annuity are you buying? How does that fit into your overall financial plan?

- What are the total fees that you will be paying when you purchase the annuity and on an annual basis?

- What restrictions and fees will I face if I need to access the funds?

- Am I being pressured into buying an annuity? When you get the contract take the time to review it as you have a ‘free look period’ and can cancel the contract within that time frame with no penalties.

- How much is the individual selling you the annuity being paid? You should never feel uncomfortable asking this question!

- Do you have an old annuity that you don’t understand or haven’t looked at for a while? Have someone aside from the person who sold it you give it a review! So many things have changed since it was sold to you that a fresh set of eyes and a second look could simply be the wisest thing you do before another mistake is made.

Over the years we have seriously spent more of our time helping clients get out of annuities than we have talking about the positive attributes associated with them. Take the time to make an informed and educated decision when considering an annuity. We often find that investors are simply not aware that building out a diversified portfolio can allow them to outperform many annuities while still providing them with the flexibility and control they desire. If you have questions or would like us to review your old annuity we would encourage you to contact us at your convenience.

Pingback: Is Financial Engines right for you? | Dear Mr. Market:

Pingback: Dear Mr. Market:

Pingback: Edward Jones: Behind the numbers and survey results | Dear Mr. Market: